Pricing the Next Wave of COPD Therapies: Lessons from Current Reimbursement Patterns

Read More

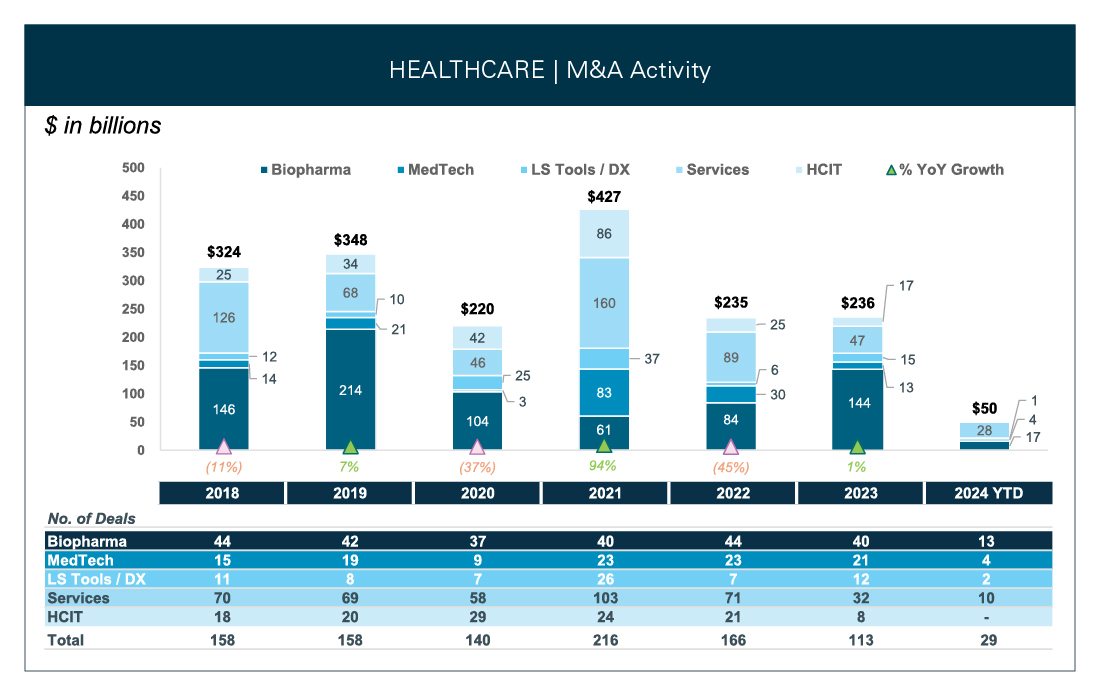

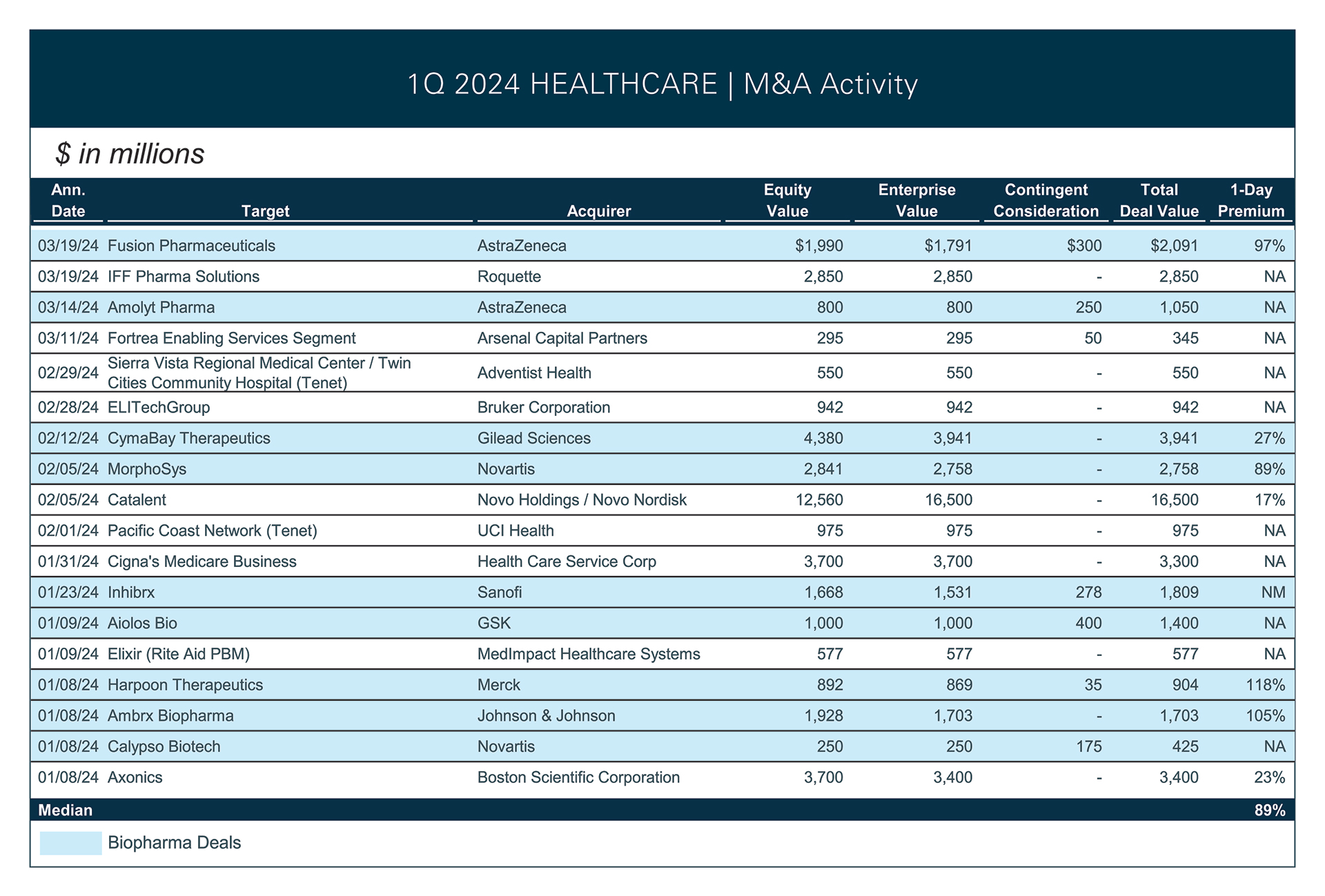

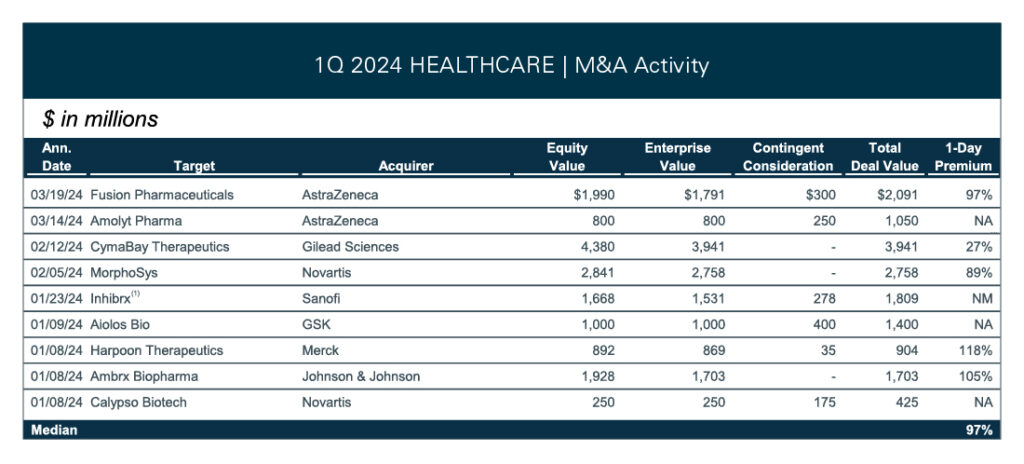

Biopharma M&A activity increased more than 100% in the first quarter of 2024 with 13 transactions in Q1 2024 compared to 6 transactions in Q1 2023. There were 47 transactions in the LTM period through March 2024 compared to 42 transactions in the LTM period through March 2023.

We expect biopharma M&A activity to remain elevated through the remainder of 2024. On the supply side, despite the rebound in the XBI and corresponding improvement in access to capital, biopharma companies will continue to seek strategic transactions as a means to access capital, accelerate program development, especially ex-U.S., and provide external validation to programs and technology. Further, as potential IPOs continue to test the market, we expect high quality companies to actively evaluate sale transactions as an alternative exit for investors. We expect distressed publicly traded companies to continue to pursue private company mergers or mergers of equals transactions. Financial buyers will remain active as a source of cash-out transactions for companies trading significantly below cash that also retain significant cash balances. On the demand side, large biopharma continues to face impending revenue gaps due to anticipated patent expiries and will continue the recent trend of targeting commercial stage or clinically de-risked companies in billion-dollar-plus deals. Larger transactions are possible, but we believe they are less likely considering FTC challenges in 2023. We expect to see significant activity away from the mega deals.

The Center for Pharmacoeconomics (“CPE”) is a division of MEDACorp LLC (“MEDACorp”). CPE is committed to advancing the understanding and evaluating the economic and societal benefits of healthcare treatments in the United States. Through its thought leadership, evaluations, and advisory services, CPE supports decisions intended to improve societal outcomes. MEDACorp, an affiliate of Leerink Partners LLC (“Leerink Partners”), maintains a global network of independent healthcare professionals providing industry and market insights to Leerink Partners and its clients. The information provided by the Center for Pharmacoeconomics is intended for the sole use of the recipient, is for informational purposes only, and does not constitute investment or other advice or a recommendation or offer to buy or sell any security, product, or service. The information has been obtained from sources that we believe reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All information is subject to change without notice, and any opinions and information contained herein are as of the date of this material, and MEDACorp does not undertake any obligation to update them. This document may not be reproduced, edited, or circulated without the express written consent of MEDACorp.

© 2026 MEDACorp LLC. All Rights Reserved.

MEDACorp has received funding to examine the potential impact of federal policies and activities on the market incentives for generic and biosimilar entry.

The Center for Pharmacoeconomics (“CPE”) is a division of MEDACorp LLC (“MEDACorp”). CPE is committed to advancing the understanding and evaluating the economic and societal benefits of healthcare treatments in the United States. Through its thought leadership, evaluations, and advisory services, CPE supports decisions intended to improve societal outcomes. MEDACorp, an affiliate of Leerink Partners LLC (“Leerink Partners”), maintains a global network of independent healthcare professionals providing industry and market insights to Leerink Partners and its clients. The information provided by the Center for Pharmacoeconomics is intended for the sole use of the recipient, is for informational purposes only, and does not constitute investment or other advice or a recommendation or offer to buy or sell any security, product, or service. The information has been obtained from sources that we believe reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All information is subject to change without notice, and any opinions and information contained herein are as of the date of this material, and MEDACorp does not undertake any obligation to update them. This document may not be reproduced, edited, or circulated without the express written consent of MEDACorp.

© 2026 MEDACorp LLC. All Rights Reserved.

MEDACorp has received funding to examine the potential impact of federal policies and activities on the market incentives for generic and biosimilar entry.

The Center for Pharmacoeconomics (“CPE”) is a division of MEDACorp LLC (“MEDACorp”). CPE is committed to advancing the understanding and evaluating the economic and societal benefits of healthcare treatments in the United States. Through its thought leadership, evaluations, and advisory services, CPE supports decisions intended to improve societal outcomes. MEDACorp, an affiliate of Leerink Partners LLC (“Leerink Partners”), maintains a global network of independent healthcare professionals providing industry and market insights to Leerink Partners and its clients. The information provided by the Center for Pharmacoeconomics is intended for the sole use of the recipient, is for informational purposes only, and does not constitute investment or other advice or a recommendation or offer to buy or sell any security, product, or service. The information has been obtained from sources that we believe reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All information is subject to change without notice, and any opinions and information contained herein are as of the date of this material, and MEDACorp does not undertake any obligation to update them. This document may not be reproduced, edited, or circulated without the express written consent of MEDACorp.

© 2026 MEDACorp LLC. All Rights Reserved.

MEDACorp has received funding to examine the potential impact of federal policies and activities on the market incentives for generic and biosimilar entry.